Microeconomics final exam cheat sheet – Prepare for success in your microeconomics final exam with this comprehensive cheat sheet. Covering fundamental principles, consumer and producer theory, market structures, and government intervention, this guide provides a concise and accessible overview of essential microeconomic concepts. Whether you’re a student seeking a quick review or a professional seeking a refresher, this cheat sheet is your ultimate resource for mastering microeconomics.

Microeconomic Concepts: Microeconomics Final Exam Cheat Sheet

Microeconomics studies the behavior of individual entities within an economy, such as consumers, producers, and firms. It analyzes how these entities make decisions and interact with each other in markets.

Fundamental microeconomic principles include supply and demand, elasticity, and market equilibrium. Supply and demand determine the prices and quantities of goods and services in a market. Elasticity measures the responsiveness of quantity demanded or supplied to changes in price. Market equilibrium occurs when the quantity supplied equals the quantity demanded.

Supply and Demand

- The law of supply states that, all other factors being equal, as the price of a good or service increases, the quantity supplied will increase.

- The law of demand states that, all other factors being equal, as the price of a good or service increases, the quantity demanded will decrease.

Elasticity, Microeconomics final exam cheat sheet

- Price elasticity of demand measures the responsiveness of quantity demanded to changes in price.

- Price elasticity of supply measures the responsiveness of quantity supplied to changes in price.

Market Equilibrium

Market equilibrium occurs when the quantity supplied equals the quantity demanded. At this point, there is no shortage or surplus of the good or service.

Consumer Theory

Consumer theory analyzes the behavior of consumers in making choices about the goods and services they purchase. It assumes that consumers are rational and seek to maximize their utility, or satisfaction.

Utility Maximization

Consumers maximize their utility by choosing the combination of goods and services that gives them the most satisfaction, given their budget constraints.

Indifference Curves

Indifference curves represent combinations of goods and services that give consumers the same level of satisfaction. Consumers prefer combinations of goods and services that are on higher indifference curves.

Factors Influencing Consumer Choices

- Income

- Prices

- Advertising

- Tastes and preferences

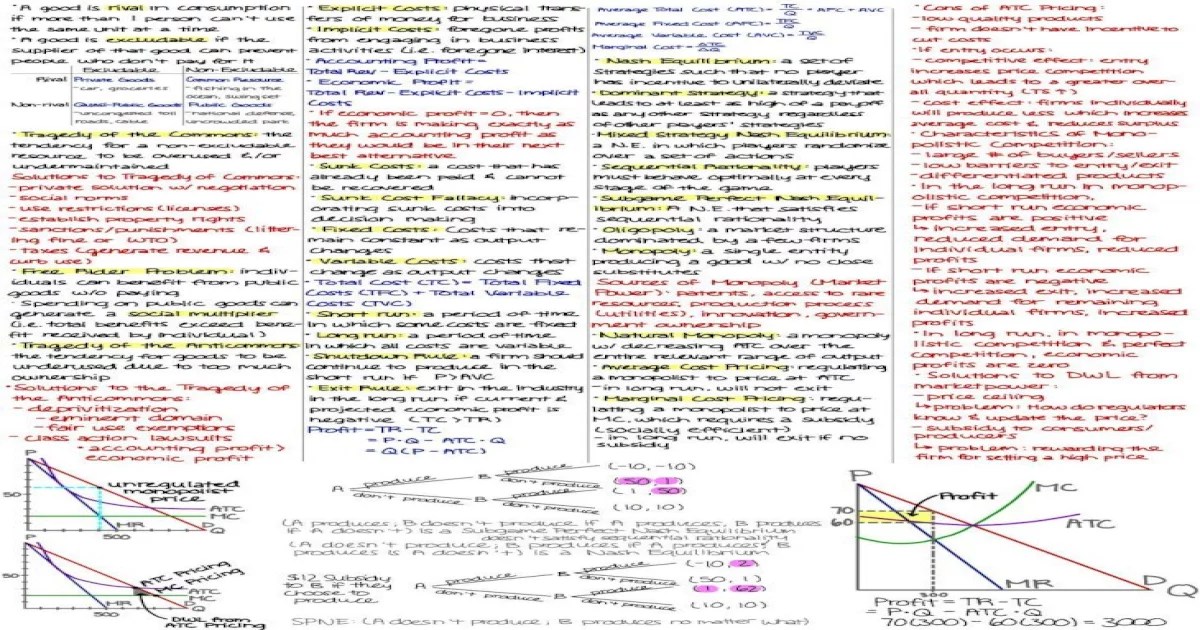

Producer Theory

Producer theory analyzes the behavior of firms in producing goods and services. It assumes that firms are profit-maximizers and seek to produce goods and services at the lowest possible cost.

Production Functions

Production functions describe the relationship between inputs (e.g., labor, capital) and outputs (e.g., goods, services).

Cost Structures

- Fixed costs are costs that do not vary with output.

- Variable costs are costs that vary with output.

- Total costs are the sum of fixed and variable costs.

Profit Maximization

Firms maximize profits by producing the quantity of output where marginal cost equals marginal revenue.

Market Structures

Market structure refers to the number and size of firms in a market and the degree of competition among them.

Perfect Competition

Perfect competition is a market structure in which there are many small firms, each producing an identical product. No single firm has market power.

Monopoly

Monopoly is a market structure in which there is only one seller of a good or service. The monopolist has complete market power.

Oligopoly

Oligopoly is a market structure in which there are a few large firms that dominate the market. Each firm has some market power.

Monopolistic Competition

Monopolistic competition is a market structure in which there are many small firms that produce differentiated products. Each firm has some market power.

Government Intervention

Government intervention in microeconomic markets can take various forms, such as price controls, taxes, and subsidies.

Price Controls

Price controls are government-imposed limits on the prices of goods and services. They can be used to protect consumers from high prices or to support producers during times of economic hardship.

Taxes

Taxes are government-imposed levies on goods and services. They can be used to raise revenue or to discourage certain behaviors, such as smoking or pollution.

Subsidies

Subsidies are government-provided financial assistance to producers. They can be used to promote certain industries or to support producers during times of economic hardship.

Applications of Microeconomics

Microeconomic principles are applied in various fields, including healthcare, education, and environmental policy.

Healthcare

Microeconomics can be used to analyze the behavior of healthcare providers, insurers, and patients. It can help policymakers design policies to improve the efficiency and effectiveness of the healthcare system.

Education

Microeconomics can be used to analyze the behavior of students, teachers, and schools. It can help policymakers design policies to improve the quality and efficiency of the education system.

Environmental Policy

Microeconomics can be used to analyze the behavior of polluters and consumers. It can help policymakers design policies to reduce pollution and protect the environment.

Questions and Answers

What are the fundamental principles of microeconomics?

Microeconomics is built on principles such as supply and demand, elasticity, and market equilibrium, which explain how individuals and firms interact in economic markets.

How does consumer behavior influence economic outcomes?

Consumer preferences, income, prices, and advertising all shape consumer choices, which in turn affect market demand and prices.

What is the role of government intervention in microeconomics?

Government policies, such as price controls, taxes, and subsidies, can influence market outcomes and address market failures or externalities.